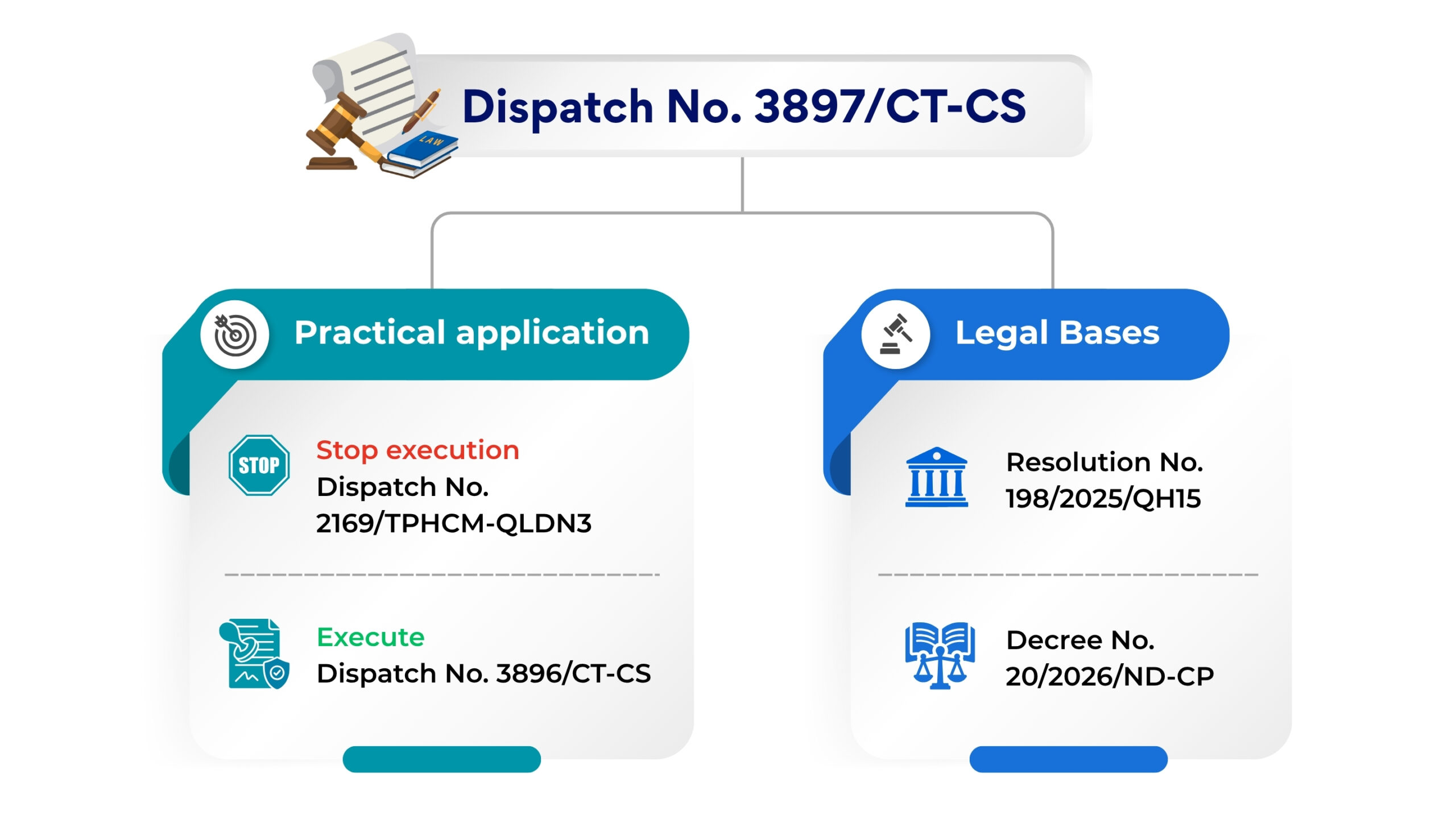

On 11/6/2026, the Tax Department issued Dispatch No. 3897/CT-CS on the corporate income tax policies pursuant to Decree No. 20/2026/ND-CP.

Accordingly, Dispatch No. 3897/CT-CS together with Dispatch No. 3896/CT-CS have clarified: foreign-funded enterprises that are established and have their operation registered in accordance with the Vietnamese are also eligible for corporate income tax for three years, provided that all the conditions applicable to small and medium enterprises who make their initial business registration have been satisfied.

In this article, CNC shall help readers to have better understanding of the necessary conditions for FDI enterprises to be eligible for this tax incentive.

Should all FDI enterprise eligible for 3-years corporate income tax exemption?

The issuance of Dispatch No. 3897/CT-CS does not give rise to a new tax incentive. The legal basis for the policy on 3-year corporate income tax exemption is mostly covered by Resolution No. 198/2025/QH15 and Decree No. 20/2026/ND-CP.

However, Dispatch No. 3897/CT-CS requires the local tax authorities to follow the instructions set forth in in Dispatch No. 3896/CT-CS, in which it is confirmed that FDI enterprises are not excluded from the policy on 3-year corporate income tax exemption simply because they involve foreign investors. In other words, FDI enterprises and foreign investors are still eligible for corporate income tax incentives, provided that all conditions in accordance with the laws have been satisfied.

Therefore, FDI enterprises and investors should exercise great care in their review of capital structure, corporate structure, and the legal history of the management team prior to the commencement.

Conditions for FDI enterprises to be eligible for corporate income tax exemption

First Condition: Obtained the initial Enterprise Registration Certificate

For small and medium enterprises who have just completed their initial business registration, they shall be eligible for corporate income tax exemption within three years of the date of issuance of the initial Enterprise Registration Certificate.

The duration of the corporate income tax exemption shall be calculated continuously from the first year of the issuance of the initial corporate income tax. Enterprises should especially take note of this issue since the absence of revenue or profits due to the delay in the operation commencement of enterprises would not automatically extend the applicable duration of the incentive. In other words, this issue has been anticipated and accounted for by the legislators so that the most reasonable approach within the economic context is adopted.

Furthermore, for those who have obtained their Enterprise Registration Certificate prior to the effective date of Resolution No. 198/2025/QH15, the tax incentive is still applicable for the remaining duration accordingly.

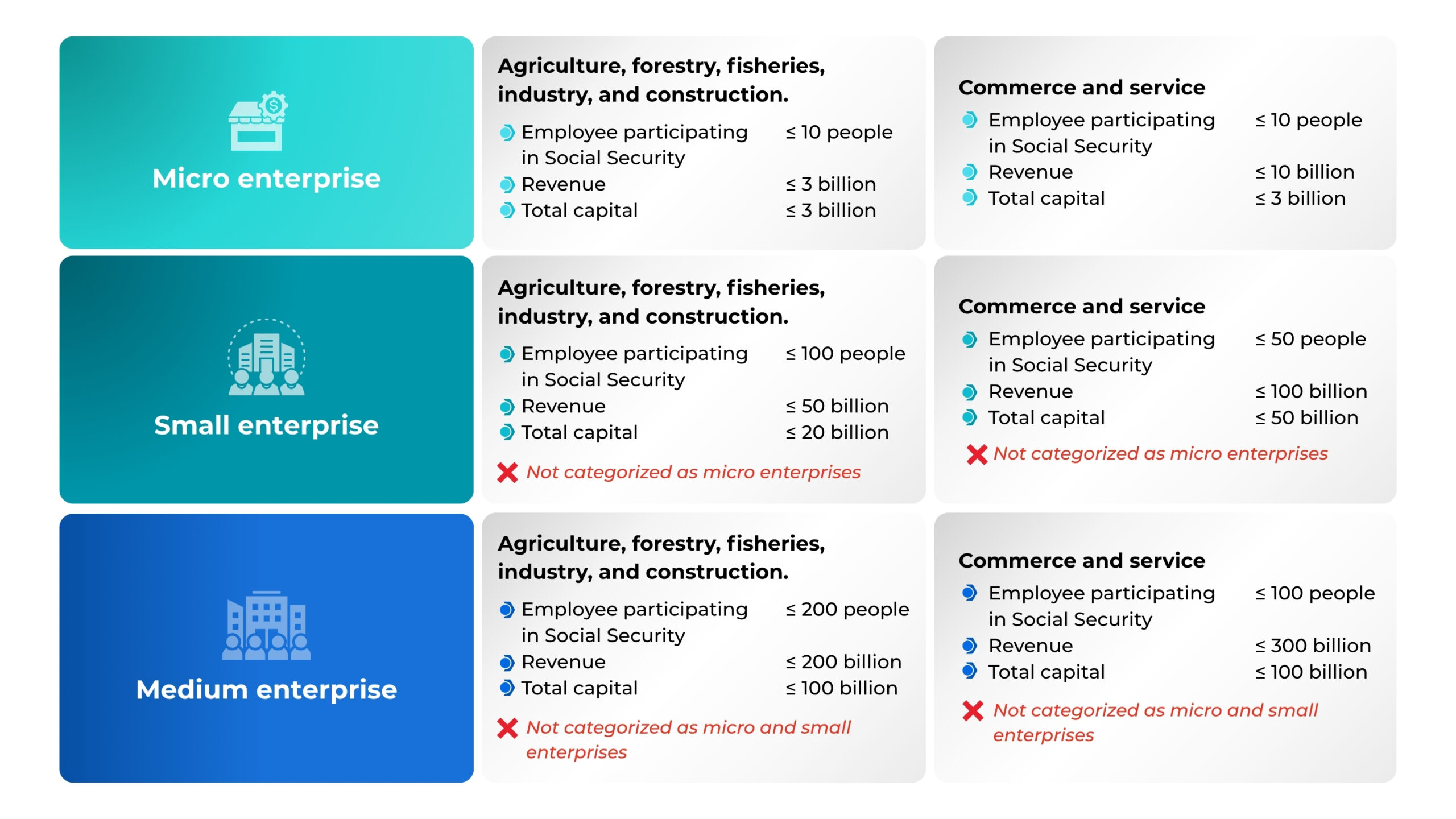

Second condition: Meet the criteria for small and medium enterprises

To be identified as small and medium enterprises, the following criteria shall be based upon:[1]

Criteria for small and medium enterprises

Third Condition: Not categorized as ineligible for the tax incentive

In addition to the second condition – meet the criteria for small and medium enterprises – enterprise must not fall within any of the following situations,[2] to be specific:

- Enterprise establishment due to merger, consolidation, division, or separation of enterprises;

- Enterprise establishment due to change in owner or enterprise models;

- Enterprises whose legal representatives, partners, or the most prominent stakeholder have participated in business activities with corresponding role at another enterprise that is currently in operation or has yet to pass its 12-month period since its dissolution;

- Some of the revenues are not eligible for the incentive in accordance with the corporate income tax laws.

Therefore, to be eligible for corporate income tax exemption, enterprises need to satisfy 03 conditions (i) Obtained the initial Enterprise Registration Certificate, (ii) Meet the criteria for small and medium enterprises, and (iii) not categorized as ineligible for the tax incentive.

Enterprises and investors must promptly take action to be eligible for the incentive

First, review/establish an appropriate capital structure from the outset

Enterprise must ensure the capital is sufficient for the operation whilst maintaining the total capital stay within the threshold determined for small and medium enterprises. Careful consideration must be made prior to any capital contribution, loan from parent companies, or high-value investment.

Second: Review and ensure an appropriate corporate structure

Enterprise must ensure the genuine recency and avoid any indication of establishment based on merger, consolidation, division, or separation of enterprises or establishment due to change in owner or enterprise model; The transfer of property, contracts, personnel or activities from the former legal person to the latter legal person must also be evaluated carefully.

Third: Review the legal history of the enterprise’s manager/owner

The legal history and role of legal representatives, partners, or the most prominent stakeholder must be reviewed. These individuals could affect the eligibility conditions if they hold a corresponding position at another enterprise that is currently in operation or has yet to pass its 12-month period since its dissolution.

Conclusion

Dispatch No. 3897/CT-CS is an important sign, indicating that the tax authorities are striving for the consistent application of the 3-year corporate income tax exemption policy for small and medium enterprises who have just completed their initial business registration.

For FDI enterprises, this is a noteworthy opportunity during the selection of investment method and establishment of legal person in Vietnam. However, the incentive is not only dependent on foreign funds, but also the capital structure, the genuine recency of the legal person, and the legal history of the management team.

Therefore, enterprises and investors should carefully research the laws, conduct practical review of the documents and consult with legal and tax experts prior to the execution to ensure that all of the eligibility conditions have been fully and consistently fulfilled.

What We Can Support?

- Inbound/Outbound Investment: Company Establishment, Investment Registration and Post-registration Services in relation to tax, accounting, labor, insurance, salary, and outsourced legal department;

- Operation Licenses: We could provide support in the application for operation licenses for business activities in fields such as manufacturing, commerce, services, e-commerce, healthcare, education, or food & beverage (restaurants);

- M&A Services: Conduct legal due diligence, structure transactions, draft and negotiate transaction documents, provide advice on competition law compliance (including merger control filings and related approvals), obtain necessary regulatory approvals and licenses, and provide post-closing support;

- Personal Data Protection: Provide support in compliance with the data protection regulations, including the drafting and reviewing of Data Protection Impact Assessment (DPIAs), Data Processing/Transfer Agreement, Privacy Policies, and other necessary documents under the Personal Data Protection Decree (PDPD);

- Dispute Resolution: Litigation and Commercial Arbitration (VIAC SIAC ICC); and

- Legal Retainer Services per the clients’ requests.

Please contact Mr. Chris Luong – Partner through the email address of chris.luong@cnccounsel.com or Ms. Ngan Nguyen – Partner through the email address of ngan.nguyen@cnccousel.com for prompt and timely support.

Managed by

|

Nguyen Thi Kim Ngan I Partner

Phone: (84) 919 639 093 Email: ngan.nguyen@cnccounsel.com |

|

Luong Van Chuong I Partner

Phone: (84) 938 04 7969 Email: chris.luong@cnccounsel.com |

|

Lam Kim long | Legal Assistant

Phone: (84) 888 210 644 Email: long.lam@cnccounsel.com |

Contact Us

For further information, please contact:

CNC Vietnam Law Firm

Address: The Rise Building, 2A1 Nguyen Thi Minh Khai, Sai Gon Ward, Ho Chi Minh City, Vietnam

Phone: (84) 28-6276 9900

Hotline: (84) 916-545-618

Email: contact@cnccounsel.com

Website: cnccounsel

We would be delighted to welcome you at CNC’s office, where you’ll have the opportunity to consult with the lawyer best suited to your circumstances. Of course, if you are unable to meet in person, simply email us via contact@cnccounsel.com or call us via (+84-28) 6276 9900.

It would be a pleasure for CNC’s lawyers to help you build a solid legal foundation, thus ensuring the success and sustainable development of your project!

————————————

Copyright © CNC Counsel. All rights reserved.

Ownership Rights: This document and the content contained herein (Document) are proprietary resources exclusively owned by CNC Counsel. Access to or use of this Document does not, by itself, create any contractual relationship or lawyer-client relationship between CNC Counsel and any person or entity.

Disclaimer: All Documents are provided solely for informational purposes and may not reflect the most current legal developments. Summaries of laws, regulations, and practices are subject to change. This Document is not intended to constitute legal, professional, or other advice with respect to any specific matter. Nor is it intended to substitute for reference to, or compliance with, the detailed provisions of any applicable law, regulation, rule, or official form. Readers are strongly encouraged to seek independent legal advice before taking, or refraining from taking, any action based on the information contained in this Document. CNC Counsel, together with its editors and authors, makes no representations or warranties as to the accuracy, completeness, or currency of the Document and disclaims all liability to any person or entity arising from reliance on all or any part of the Document. This Document may contain links to external websites, and external websites may contain links to this Document. CNC Counsel is not responsible for the content, operation, availability, or practices of any such external websites and expressly disclaims any liability in connection therewith. Note: Past results do not guarantee similar outcomes in future matters. Each matter is unique and must be assessed based on its own facts and circumstances.

————————————

[1] Article 5 Decree No. 80/2021/ND-CP on guidelines for Law on Support for small and medium enterprises.

[2] Point b, Clause 3, Article 7, Decree No. 20/2026/ND-CP.