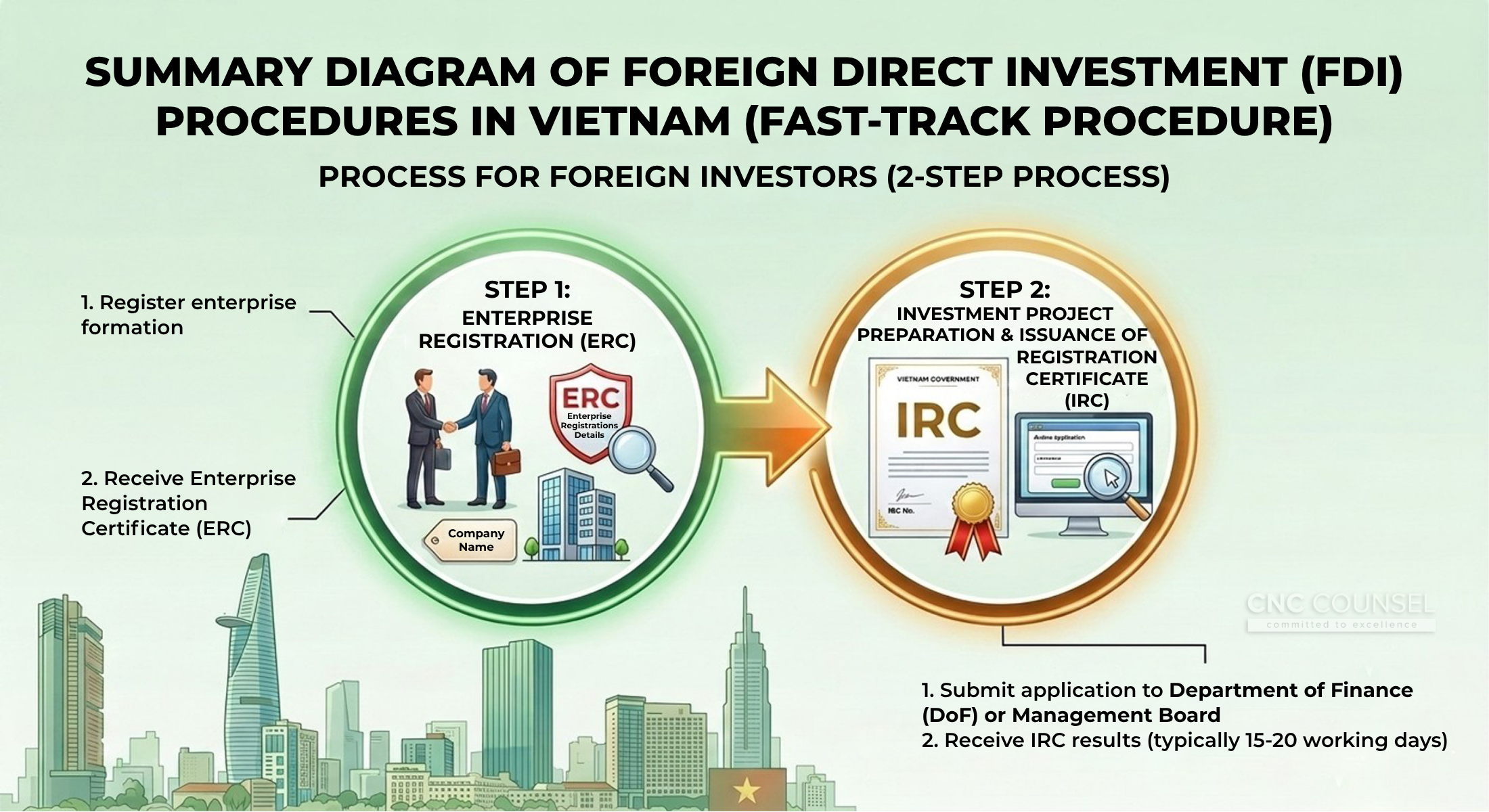

Innovative Mechanism: ERC First, IRC Later

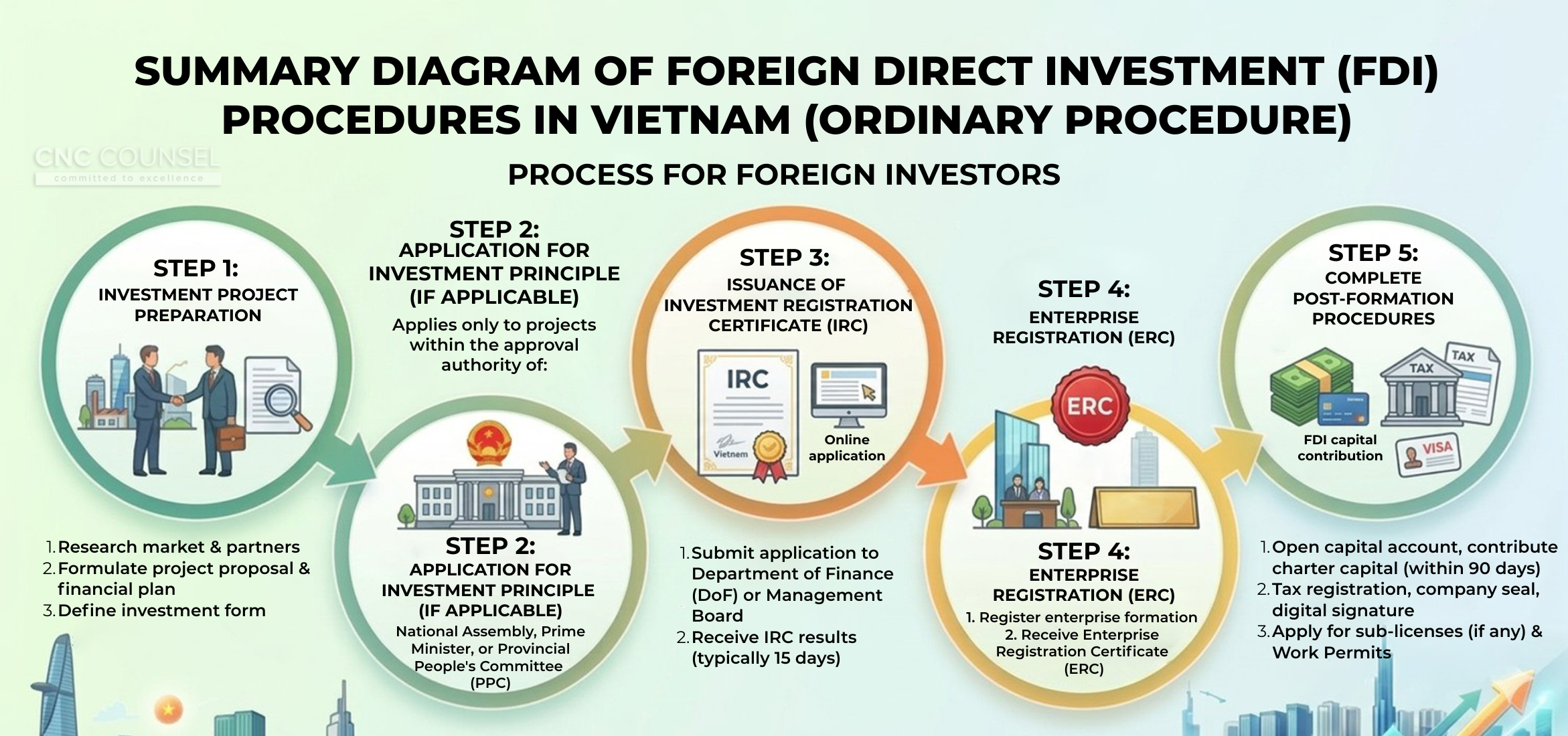

Under the old process, foreign investors were required to obtain the Investment Registration Certificate (IRC) before establishing a business and receiving the Enterprise Registration Certificate (ERC). The Investment Law 2025 (effective from March 1, 2026) and Decree 96/2026/ND-CP (effective from March 31, 2026) introduce a new mechanism: foreign investors can establish a business first and then complete the IRC issuance procedures within 12 months thereafter. The practical goal of this new mechanism is to allow investors to sign office/factory lease contracts, hire initial staff, and prepare internal procedures without waiting for the IRC.

The “ERC-first, IRC-later” mechanism only applies to cases not requiring Investment Policy Approval (IPA) or projects not requiring an IRC. Therefore, projects requiring IPA (e.g., large-scale land use projects, key infrastructure, sensitive sectors, etc.) must still follow the old sequence: IPA, IRC, ERC.

Official Letter No. 5427/BTC/DNTN issued by the Ministry of Finance on April 29, 2026, provides more specific guidance for investors and nationwide business registration agencies on the sequence and procedures for applying the “ERC-first, IRC-later” mechanism. Accordingly, if investors apply this mechanism, the Enterprise Registration Application must include the investor’s commitment to meet market access conditions under Article 8 of the Investment Law 2025. This is the investor’s self-commitment—the business registration agency does not verify this content at the time of issuing the ERC. After obtaining the ERC, the enterprise cannot add business lines related to the project until it has the IRC.

Foreign Direct Investment Capital Account (DICA): A Key Bottleneck

Currently, Circular 06/2019/TT-NHNN still requires FDI enterprises to open a DICA after obtaining the IRC. This creates a practical gap when the enterprise has an ERC but no IRC yet, potentially preventing it from opening a DICA and contributing charter capital or investment capital through official channels.

However, this bottleneck is being addressed by the State Bank of Vietnam (SBV) to align with the Investment Law 2025 and compatibility with the “ERC-first, IRC-later” mechanism. Accordingly, the SBV is currently soliciting comments on a draft Circular to replace Circular 06/2019/TT-NHNN, with the key point allowing enterprises to open DICA and conduct certain transactions before having the IRC—including receiving initial capital contributions and paying project formation costs. The draft also relaxes account limits, such as allowing multiple foreign currency accounts of different currencies at the same bank, and lowering the FDI enterprise threshold from “over 51%” to “over 50%” of charter capital.

However, note that until the Draft is officially issued, commercial banks may still require investors to have an IRC before allowing DICA opening. Therefore, investors should confirm specifically with the intended commercial bank and advisors before registering the business establishment.

Legal Consequences of Failure of IRC Obtainment Within the Statutory Period When Applying the “ERC-First, IRC-Later” Mechanism

Decree 96/2026/ND-CP guiding the Investment Law 2025 requires foreign investors to complete IRC procedures within 12 months from the date of ERC issuance but does not specify legal consequences or handling mechanisms if investors violate (or fail to do so). This will create legal and procedural uncertainty for both investors and licensing agencies. Under the current legal framework, unclear issues may include: whether the ERC remains valid, whether the enterprise will be required to dissolve, or whether competent authorities can revoke the ERC by administrative decision if the foreign investor does not (or cannot) complete the IRC procedures within 12 months from ERC issuance.

This lack of clarity will certainly complicate activities and agreements related to the economic organization/investor, such as shareholder agreements, capital contribution schedules, financial contracts, and operation contracts, and may lead to inconsistent approaches among local agencies.

General provisions from the Investment Law 2025 and previous guiding Decrees (such as Decree 31/2021) indicate that the State may impose administrative fines or revoke previously issued licenses for acts such as “not implementing the project” or “ceasing operations”. Although the ERC remains valid under the Enterprise Law, lack of IRC leading to non-implementation of the investment project may result in administrative penalties under the Decree on administrative sanctions in the investment sector.

We can look to some Southeast Asian jurisdictions with similar regulations for reference:

- Indonesia had a similar issue and resolved it transparently. Investors register foreign-invested companies (PT PMA) first, then complete investment procedures via the online system (OSS) within the prescribed period; if not, they may face fines or cancellation of investment registration, similar risks to Vietnam.

- In Thailand, investors can establish companies first through the Department of Business Development under the Thai Ministry of Commerce (DBD), but then need to apply for a Foreign Business License or Board of Investment promotion for certain regulated sectors; if not completed, the company may be restricted from operations, face administrative fines, or business suspension, without automatic dissolution.

- In Malaysia, investors can register companies first through the Companies Commission of Malaysia (SSM), then seek approval letters from the Malaysian Investment Development Authority (MIDA) for investment projects. This country allows more flexible timelines, with legal consequences mainly being denial of investment incentives or revocation of project licenses if delayed, without directly affecting the project company’s existence.

- Myanmar follows a discretionary approach with specified legal consequences. Myanmar’s Investment Law provides for administrative penalties, including suspension of investment incentives or even revocation of issued licenses. However, Myanmar does not have a specific deadline like Vietnam, and application is highly discretionary.

The above information shows that clarifying the legal consequences of violating investment registration procedures is essential and legally feasible to ensure stability in the business environment. Additionally, experiences from Indonesia, Thailand, and Malaysia suggest that appropriate legal consequences should focus on denying investment incentives, requiring the company to cease operations, or administrative fines, rather than directly affecting the project company’s existence (e.g., mandatory enterprise dissolution). These are issues that Vietnam will need clearer guidance and resolution in the near future.

Recommendations

The “ERC-first, IRC-later” mechanism is suitable for investors needing to shorten preparation and business operation launch time (such as signing premises leases, hiring staff, etc.) while finalizing IRC documents in parallel.

However, kindly note that for (i) projects requiring Investment Policy Approval (IPA), or (ii) until a new official Circular allows enterprises to open DICA before issuance of IRC to fit the “ERC-first, IRC-later” mechanism (at the time of this article, the new Circular is only in Draft form), the traditional IRC → ERC → DICA registration sequence remains the most legally secure path.

Additionally, due to unclear legal consequences if IRC is not (or cannot be) completed within 12 months after ERC issuance, investors should include conditions precedent or termination clauses in contracts/agreements signed during the IRC waiting period to handle risks if IRC is not granted later.

Copyright © CNC Counsel. All rights reserved. Ownership: This documentation and content (Content) is a proprietary resource owned exclusively by CNC Counsel. Use of this Content does not of itself create a contractual relationship, nor any attorney/client relationship, between CNC Counsel and any person. Disclaimers: The Content provided is for informational purposes only and may not reflect the latest legal or regulatory developments. Summaries of laws, regulations, and practices are subject to change. This Content does not constitute legal or professional advice for any specific situation and should not be relied upon as a substitute for reviewing and complying with applicable laws, rules, regulations, or official forms. Always seek legal counsel before making any decisions or taking any action based on this Content. CNC Counsel, along with its editors and contributing authors, make no guarantees regarding the accuracy of the Content and explicitly disclaim any liability for any consequences resulting from actions taken, allowed, or omitted, whether fully or partially based on any part of the Content. The Content may include links to external websites, and external sites may also link to it. CNC Counsel is not responsible for the content or functionality of any such external websites and disclaims all liability for any issues arising from their content or operation. Please note: Past results do not guarantee similar outcomes.

Managed by

|

Chuong Van Luong I Partner

Phone: (84) 938 04 7969 Email: chris.luong@cnccounsel.com |

Contact Us

For further information, please contact:

CNC Vietnam Law Firm

Address: The Rise Building, 2A1 Nguyen Thi Minh Khai, Sai Gon Ward, Ho Chi Minh City, Vietnam

Phone: (84) 28-6276 9900

Hotline: (84) 916-545-618

Email: contact@cnccounsel.com

Website: cnccounsel

We would be delighted to welcome you at CNC’s office, where you’ll have the opportunity to consult with the lawyer best suited to your circumstances. Of course, if you are unable to meet in person, simply email us via contact@cnccounsel.com or call us via (+84-28) 6276 9900.

It would be a pleasure for CNC’s lawyers to help you build a solid legal foundation, thus ensuring the success and sustainable development of your project!